Rwanda’s new transfer pricing order, published on 29 April 2026, creates a simple practical problem for finance leaders: if the tax administration asks for documentation, seven days is not enough time to build a defensible file from scratch.

That is the point CFOs should not miss. The new rules are not only about having a transfer pricing policy. They are about whether a company can explain, evidence, and defend its related-party pricing before the pressure of a tax query begins.

For companies with group transactions, cross-border services, shareholder financing, management fees, distribution structures, or dealings involving low-tax jurisdictions, transfer pricing is now less of a year-end tax file and more of a standing finance-control issue.

Key Takeaways

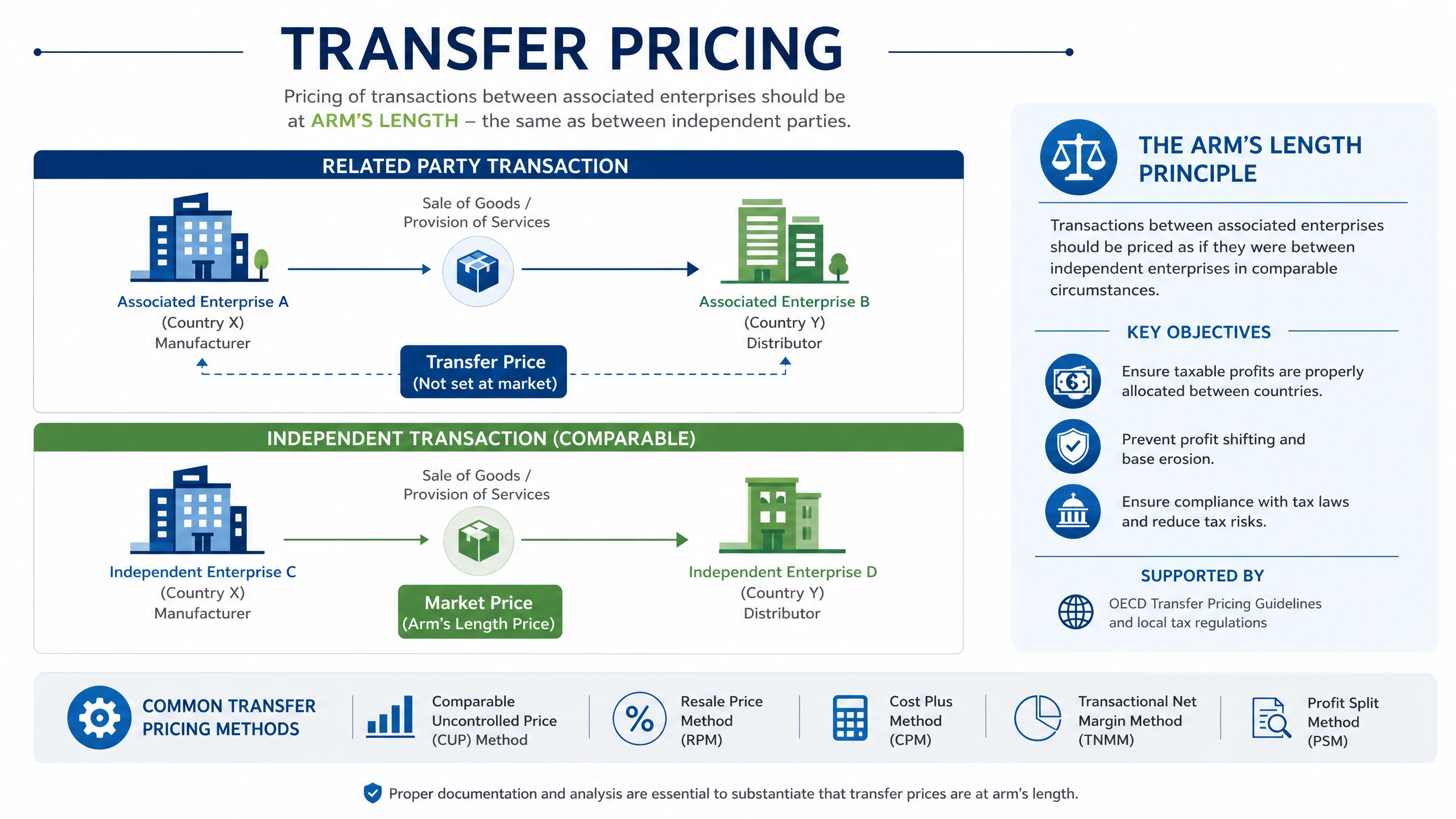

- Rwanda’s new transfer pricing framework applies the arm’s length principle to controlled transactions and certain dealings involving beneficial tax regimes.

- The seven-day response window makes transfer pricing a readiness issue, not a file to reconstruct after an RRA request.

- Smaller taxpayers may avoid the full documentation package, but they still need pricing that can be defended as arm’s length.

- RRA can look beyond the amount charged and, in serious cases, challenge whether the transaction reflects commercial reality.

- Advance Pricing Agreements may help larger taxpayers with recurring high-value transactions, but only where the facts are stable and well documented.

The Real Change Is Readiness

Ministerial Order No. 003/26/10/TC of 29 April 2026 sets out Rwanda’s transfer pricing rules in greater operational detail. It covers controlled transactions, recognised pricing methods, documentation, exemptions, country-by-country reporting, and Advance Pricing Agreements. The order came into force on the date of publication.

But the most important business implication is not the length of the order. It is the readiness standard it creates.

A company can no longer assume that transfer pricing documentation is something to assemble once a dispute starts. Under Article 18, upon written request by the tax administration, the taxpayer provides the documentation within seven days from receipt of the request, with specific exceptions for certain documents submitted with the tax declaration.

Finance teams therefore need current files, aligned contracts, clear transaction maps, and evidence that reflects how the business actually operates.

That is why this is a CFO issue, not only a tax-department issue.

Jurisdiction Risk Now Matters, Even Beyond Related Parties

The order applies where one party is in Rwanda and the other related party is in or outside Rwanda. That will be familiar to companies with multinational group structures.

The wider point is that the order also covers certain transactions involving jurisdictions considered to provide beneficial tax regimes, whether the parties are related or not.

That expands practical risk analysis. Finance teams cannot only ask, “Is this a related party?” They also need to ask:

- Where is the counterparty located?

- Is the jurisdiction low-tax or preferential?

- Does the arrangement have enough commercial substance?

- Can the company explain why the pricing reflects independent-party behaviour?

The order treats a jurisdiction as beneficial where, among other things, it does not tax income or taxes it at a maximum of 15%, grants tax breaks to non-residents, does not require substantial economic activity, or restricts access to ownership and structure information.

For CFOs, that means jurisdiction risk and substance risk now sit closer to transfer pricing risk.

RRA Can Challenge More Than The Price

The order allows the tax administration to disregard a controlled transaction where the arrangement differs from what independent parties acting commercially would have agreed and where that difference prevents the determination of an arm’s length price.

In practical terms, RRA is not limited to asking whether a management fee, loan interest rate, service charge, or royalty is too high or too low. In serious cases, the authority may challenge whether the arrangement itself reflects commercial reality.

That makes the quality of the underlying business explanation important. Contracts matter, but conduct matters too. If the contract says one thing and the operating facts show another, the file is already exposed.

Documentation Must Explain The Business, Not Just The Calculation

The order recognises standard transfer pricing methods, including comparable uncontrolled price, resale price, cost plus, transactional net margin, and transactional profit split. It also allows an alternative method where appropriate.

For CFOs, the important point is not to memorise the method names. It is that method selection must be defensible. A strong file should explain what each party does, what risks each party bears, what assets used, why the method was selected, and how the pricing outcome was tested.

This is where many companies underestimate the burden. Transfer pricing documentation is not just a tax calculation. It is a structured explanation of the business.

The Exemption Threshold Is Helpful, But Not A Safe Harbour

Article 19 exempts some taxpayers from preparing the full documentation package where annual turnover is below FRW 600,000,000 and controlled transactions are below FRW 10,000,000 per transaction or below FRW 100,000,000 in aggregate.

That exemption is useful, but CFOs should be careful with how they interpret it. The exemption is from preparing full documentation. It is not an exemption from the arm’s length principle itself.

A smaller company with related-party loans, shared services, group support costs, or recurring cross-border charges should still keep enough evidence to explain the commercial logic of its pricing.

When An APA Is Worth Considering

The first question is not whether an Advance Pricing Agreement is available. It is whether the transaction is material, recurring, and predictable enough to justify seeking advance certainty.

The order formalises APAs for eligible taxpayers, including those with controlled transactions of at least FRW 100,000,000 and annual turnover of at least FRW 600,000,000. It also provides for a non-refundable processing fee of FRW 6,000,000.

An APA may be valid for three years and may be renewed once. A taxpayer may also request rollback to one or more prior tax years, up to two years before the APA term, subject to the applicable conditions.

For companies with recurring high-value transactions, an APA can provide more certainty. But it is not a quick administrative fix. It requires reliable facts, strong documentation, and annual compliance reporting.

What CFOs Should Fix Before The Request Arrives

The first priority is to know the transaction population. Finance teams should map related-party and high-risk cross-border transactions, including services, financing, procurement, distribution, intellectual property, shared costs, and dealings with preferential jurisdictions.

The second priority is to test the response file. If RRA asked today, could the company produce the relevant documents, contracts, analysis, and financial support within seven days?

A practical readiness review should ask:

- Which transactions are in scope?

- Which entities or counterparties create jurisdiction or substance risk?

- Do contracts match the conduct of the parties?

- Is there a current local file where one is required?

- Can the company explain the selected method and comparables?

- Are finance, legal, tax, and operations working from the same facts?

- Is the company a candidate for an APA, or does it first need documentation cleanup?

A Governance Signal, Not Just A Tax Update

The April 2026 transfer pricing rules point to a more documentation-led tax environment in Rwanda. As the economy becomes more connected to regional groups, investment structures, financial institutions, and cross-border service models, tax administration will naturally pay closer attention to how value is priced and evidenced.

For CFOs, the lesson is not to panic. It is to prepare.

Companies that can explain their related-party pricing clearly, support it with evidence, and respond quickly will be in a stronger position with tax authorities, auditors, lenders, investors, and boards.

Seven days is not enough time to create transfer pricing discipline. It is enough time to reveal whether that discipline already exists.

If your organisation has material related-party or cross-border arrangements, the practical next step is a transfer pricing readiness review before a request arrives.